Calibration alternatives to logistic regression and their potential for transferring the statistical dispersion of discriminatory power into uncertainties in probabilities of default - Journal of Credit Risk

Por um escritor misterioso

Last updated 21 setembro 2024

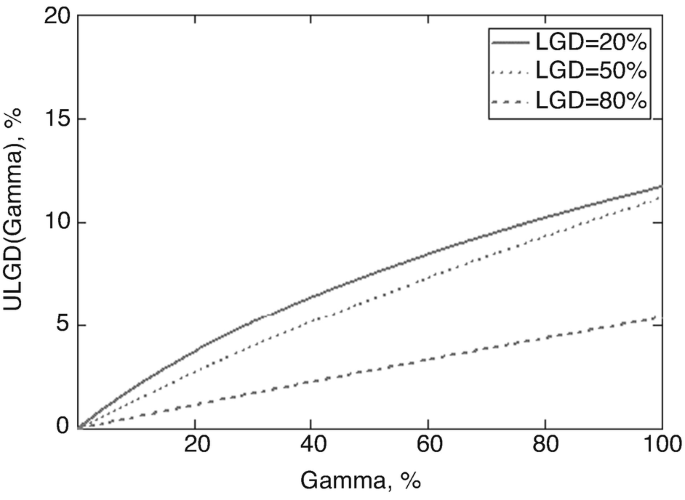

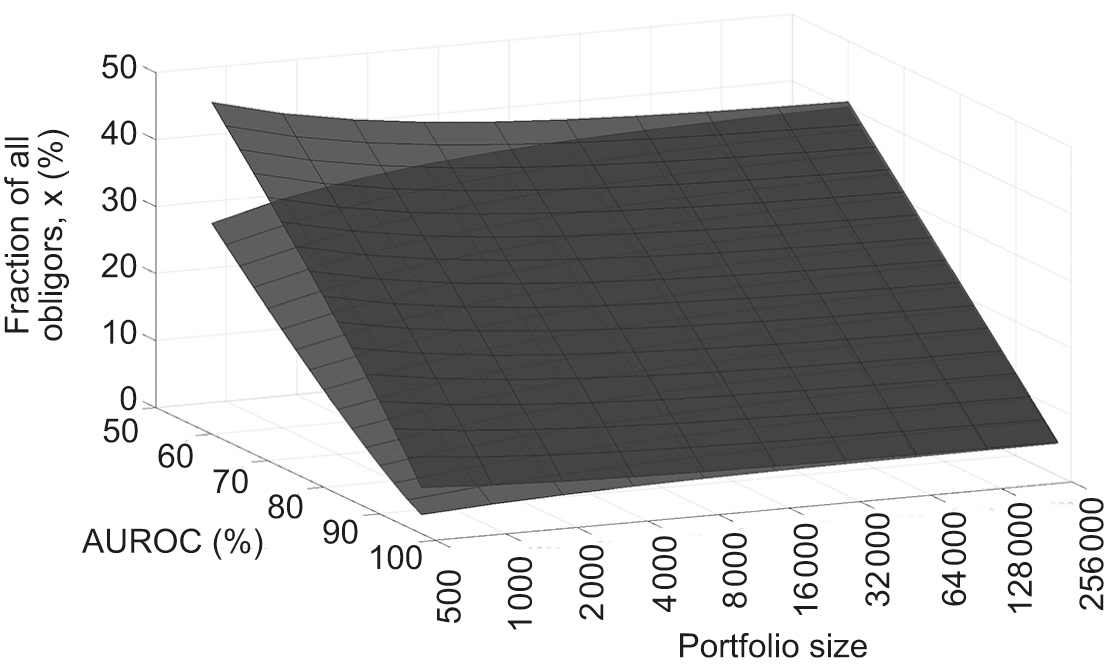

This paper compares four calibration approaches to linear logistic regression in credit risk estimation and proposes two new single-parameter families of

How to interpret weights in logistic regression - Quora

Loss Given Default Estimations in Emerging Capital Markets

Exposure at default models with and without the credit conversion

The instability in logistic regression

Risks, Free Full-Text

Calibration alternatives to logistic regression and their

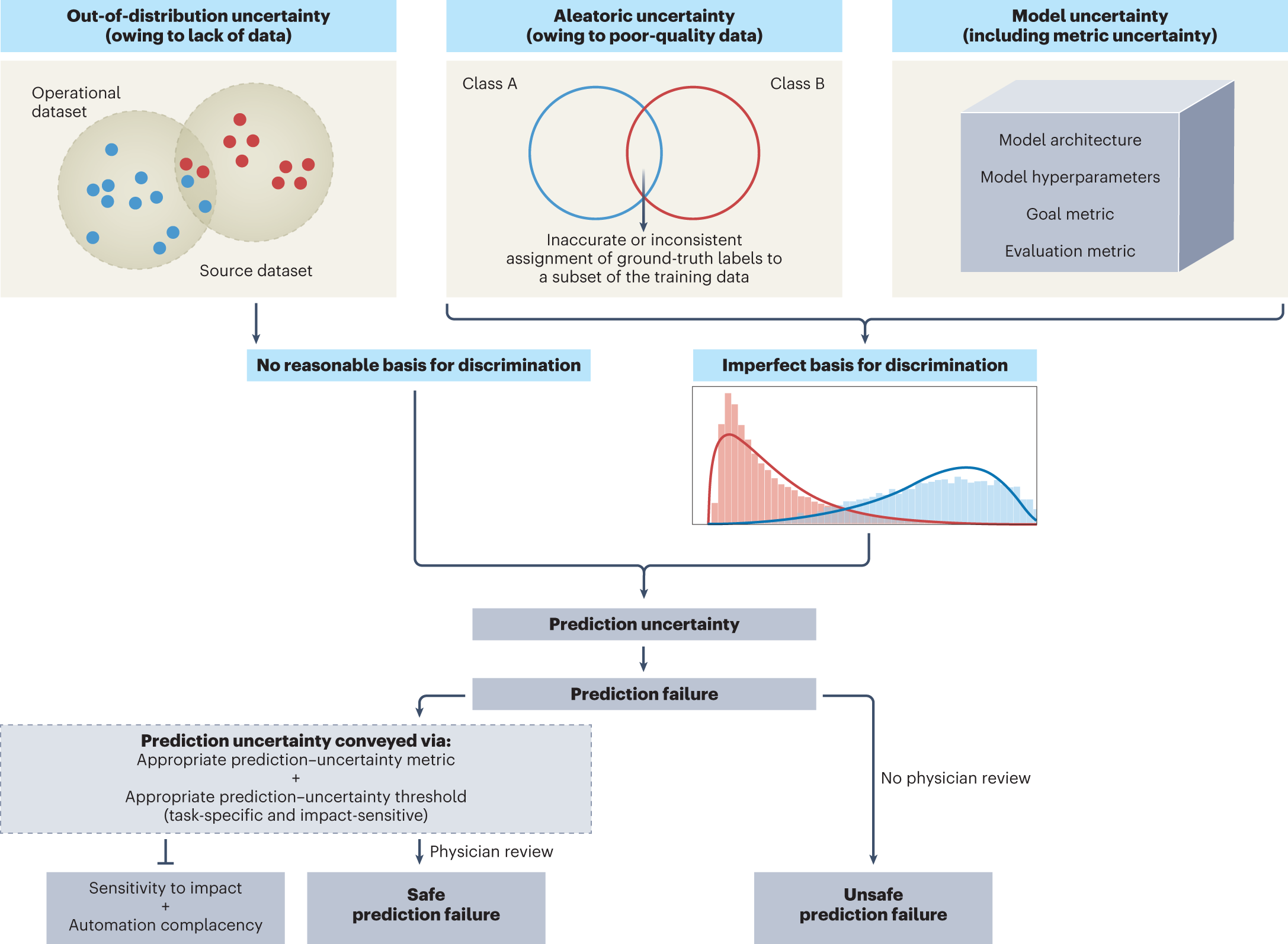

Tackling prediction uncertainty in machine learning for healthcare

A mixture model for credit card exposure at default using the

What are the assumptions required for linear regression and

Recomendado para você

-

Clique aqui para download - Caruana Financeira21 setembro 2024

Clique aqui para download - Caruana Financeira21 setembro 2024 -

Caruana S.A. Sociedade de Credito, Financiamento e Investimento21 setembro 2024

-

File:Caruana, Jaime (IMF 2008) (frame).jpg - Wikimedia Commons21 setembro 2024

File:Caruana, Jaime (IMF 2008) (frame).jpg - Wikimedia Commons21 setembro 2024 -

Brazil Lending Rate: per Annum: Pre-Fixed: Corporate Entities: Vendor: Banco Cedula S.A., Economic Indicators21 setembro 2024

-

Certification - OpenID Foundation21 setembro 2024

Certification - OpenID Foundation21 setembro 2024 -

Water, Free Full-Text21 setembro 2024

Water, Free Full-Text21 setembro 2024 -

Probability diagram of the nursing diagnosis.21 setembro 2024

Probability diagram of the nursing diagnosis.21 setembro 2024 -

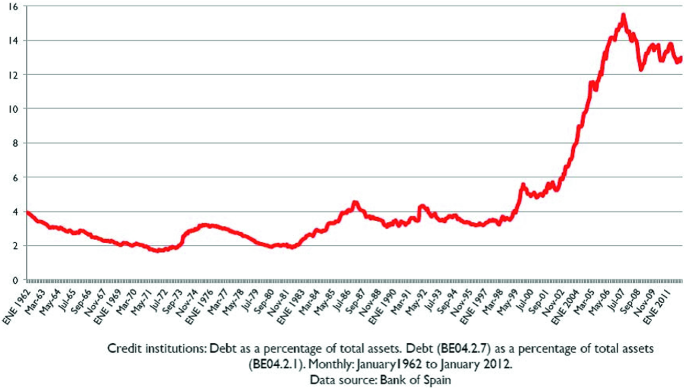

The Global Financial Crisis and the Spanish Banking System: Explaining Its Initial Success (2007–2010)21 setembro 2024

The Global Financial Crisis and the Spanish Banking System: Explaining Its Initial Success (2007–2010)21 setembro 2024 -

Homeownership, mobility, and unemployment: Evidence from housing privatization - ScienceDirect21 setembro 2024

Homeownership, mobility, and unemployment: Evidence from housing privatization - ScienceDirect21 setembro 2024 -

Daily Schedules - Federal Reserve Bank of New York21 setembro 2024

Daily Schedules - Federal Reserve Bank of New York21 setembro 2024

você pode gostar

-

Coaldale Block street pavers line a walkway at Spring Hill College, Aug. 22, 2020, in Mobile, Alabama. The red clay bricks were made by Coaldale Brick Stock Photo - Alamy21 setembro 2024

Coaldale Block street pavers line a walkway at Spring Hill College, Aug. 22, 2020, in Mobile, Alabama. The red clay bricks were made by Coaldale Brick Stock Photo - Alamy21 setembro 2024 -

EA Play 6 Month Subscription (Xbox One/ Xbox Series S|X) Key GLOBAL21 setembro 2024

EA Play 6 Month Subscription (Xbox One/ Xbox Series S|X) Key GLOBAL21 setembro 2024 -

![42+] Punisher HD Wallpaper](https://cdn.wallpapersafari.com/61/88/1gEukh.png) 42+] Punisher HD Wallpaper21 setembro 2024

42+] Punisher HD Wallpaper21 setembro 2024 -

![Raikou (Cracked Ice Holo) (16) [Miscellaneous Cards & Products] – Pokemon Plug](https://pokemonplug.com/cdn/shop/products/153238.jpg?v=1660587375) Raikou (Cracked Ice Holo) (16) [Miscellaneous Cards & Products] – Pokemon Plug21 setembro 2024

Raikou (Cracked Ice Holo) (16) [Miscellaneous Cards & Products] – Pokemon Plug21 setembro 2024 -

Play Super Mario World Online – Super Nintendo(SNES) –21 setembro 2024

Play Super Mario World Online – Super Nintendo(SNES) –21 setembro 2024 -

Goblin Slayer (@GoblinSlaying) / X21 setembro 2024

Goblin Slayer (@GoblinSlaying) / X21 setembro 2024 -

Street Fighter Alpha Anthology Ps2 (Jogo Original) (Seminovo) - Arena Games - Loja Geek21 setembro 2024

Street Fighter Alpha Anthology Ps2 (Jogo Original) (Seminovo) - Arena Games - Loja Geek21 setembro 2024 -

shinka no mi: shiranai uchi ni kachigumi jinsei dublado21 setembro 2024

shinka no mi: shiranai uchi ni kachigumi jinsei dublado21 setembro 2024 -

Vaquejada Gamer transforma prática cultural do Nordeste em jogo de21 setembro 2024

Vaquejada Gamer transforma prática cultural do Nordeste em jogo de21 setembro 2024 -

Crunchyroll to Stream Technoroid Overmind, High Card, Nijiyon, The Angel Next Door Spoils Me Rotten, More Anime - News - Anime News Network21 setembro 2024

Crunchyroll to Stream Technoroid Overmind, High Card, Nijiyon, The Angel Next Door Spoils Me Rotten, More Anime - News - Anime News Network21 setembro 2024